Australia’s superannuation system is about to get its biggest shake-up in decades — and for millions of workers, that could mean thousands of dollars more in their retirement savings.

The Albanese government has announced a bold new plan called Payday Super, which would force employers to pay your super every time you’re paid — not just once every few months.

The idea sounds simple, but it’s set to spark a nationwide shift in how money moves between employers, workers, and the tax office. And while Labor says it’ll help workers retire richer, small businesses warn it could squeeze cash flow and pile on new admin pressure.

Let’s break down what this all really means — and how much extra you could end up with.

What Exactly Is Payday Superannuation?

Right now, most employers pay super quarterly, which means your retirement money can sit unpaid for months — or, worse, never get paid at all if the company goes under or simply doesn’t comply.

Treasurer Jim Chalmers wants to change that. Under the proposed Payday Super law, your employer would have to deposit super into your fund within seven days of each payday.

He says it’s about fairness and helping Australians get the full benefit of compounding returns.

Employees will benefit from more frequent and earlier super contributions that will grow and compound over their working life, Chalmers said.

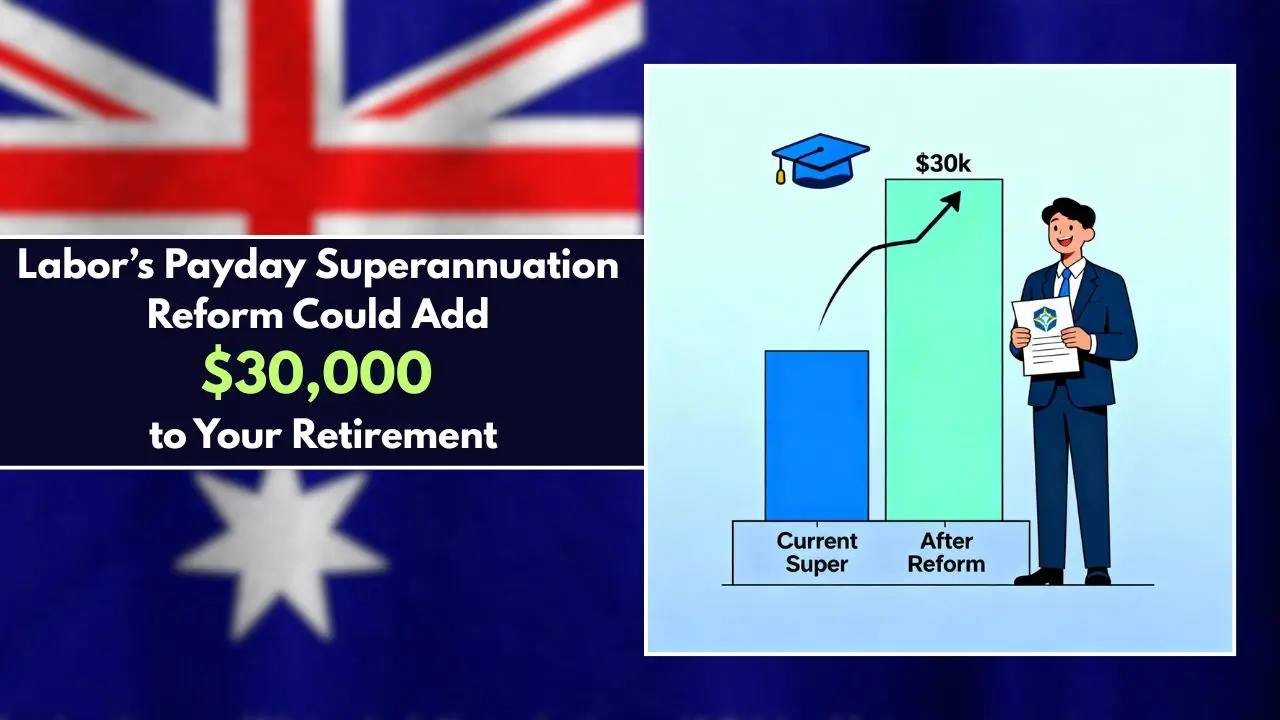

According to Treasury, a 25-year-old worker could retire with $6,000 more just from the new payment schedule alone. And for anyone who’s missed super payments entirely, recovering them could boost their retirement balance by more than $30,000 in today’s dollars.

Why the Government Is Cracking Down

Unpaid super is a huge problem. The Australian Taxation Office (ATO) estimates that employers failed to pay around $5.2 billion in super last financial year.

That’s not pocket change — it’s money that should have been earning investment returns for workers’ futures. And it’s not evenly spread: women, part-time workers, and casual employees are often the hardest hit.

By linking super payments directly to payday, the government hopes to cut down on unpaid super, make it easier for the ATO to detect non-payment quickly, and help employees build up savings faster.

When Will the New Rules Start?

If the law passes Parliament, Payday Super will kick in from July 1, 2026.

That gives employers about 18 months to get ready — update payroll systems, tweak cash-flow schedules, and prepare for more frequent payments.

Why Some Businesses Aren’t Happy

While most workers have cheered the move, not everyone’s thrilled.

CPA Australia, one of the country’s largest accounting bodies, has warned that smaller employers may struggle to adjust.

Some small businesses will face significant cash-flow challenges as they adjust to the new regime, said Richard Web, CPA Australia’s superannuation lead.

He said that while the ATO has offered an assisted compliance period to ease the transition, that’s not the same as giving businesses formal time to adapt under the law.

This may be another compliance headache that many small businesses will struggle to cope with in such a short space of time, he added.

How Much Extra Money Could Workers Gain?

The magic lies in compound growth.

When your employer pays super more often, the money starts earning returns sooner. Over years, that small timing difference adds up.

Here’s what Treasury modelling shows:

- 25-year-old on $70,000/year: around $6,000 extra in retirement.

- 35-year-old who recovers unpaid super: roughly $30,000 more saved.

It’s not about getting more contributions — it’s about getting them faster, so the investment clock starts ticking earlier.

What It Means for Employers

Once the law takes effect, businesses will need to:

- Pay super within seven business days after each payday.

- Update payroll systems to automatically calculate and send super contributions.

- Report payments in real time so the ATO can track compliance.

Larger companies already using automated payroll software may find the switch easy. But smaller businesses — especially those relying on manual processes — will need upgrades, planning, and possibly new accounting help.

Could This Reform Backfire?

Economists say there’s a balancing act here.

On one hand, Payday Super ensures billions flow more steadily into the $3.5 trillion superannuation sector, giving workers stronger long-term growth.

On the other, it could create short-term pain for small employers, especially in industries like hospitality, construction, and retail where wages make up a big chunk of expenses.

That’s why CPA Australia and other business groups want clear guidance, flexible rollout timelines, and fair penalties for first-time non-compliance.

The Bigger Picture: Fairer Retirement, Fewer Loopholes

The government says this isn’t just about payroll rules — it’s about closing the gap between what Australians earn and what they actually retire with.

Too many Australians — especially women and casual workers — have been short-changed on their super for too long, Chalmers said.

By ensuring super is paid in sync with wages, Labor hopes to deliver a fairer, more transparent system that protects workers’ futures.

Overall Summary

If the Payday Super laws pass, Australians could retire with thousands more in their accounts — especially younger workers and those in casual jobs.

For employers, it means faster payments, new systems, and tighter compliance — but also a cleaner, more transparent way to manage obligations.

With unpaid super still topping $5 billion a year, this reform could be one of the most meaningful changes to the nation’s retirement system in decades.

The bill is set to roll out from July 1, 2026 — and every Australian should be paying attention.

About the Author

Elias Vennor is a professional writer and editor at EPfortal.com, specializing in Finance and Trending Topics. With a strong background in content research and journalism, Elias Vennor is dedicated to delivering accurate, well-sourced, and timely information to help needy peoples. Their articles follow strict editorial standards, relying on official sources and verified data to ensure credibility. Covering the latest Finance and more related Topics, Elias Vennor aims to make Updated information accessible and easy to understand for all readers.

No Comments Yet

Be the first to share your thoughts.

Leave a Comment